Banks aren't in the retail industry; they are essential

services you can't function without. They should be non-profit to avoid the inherent

conflict of interest and they need to be to actively regulated.

The main reason banks tells us we need a credit card is to

establish a credit rating. The main reason for establishing a credit rating is

for getting loans from banks who give out the credit cards. Notice a problem?

It’s a vicious pressure cycle of debt for profit.

Banks were created to eliminate loan sharks and to lubricate

and stabilize the financial system. Banks should be financial only through

deposits, loan interest, and bonds. No stocks. Issuing stocks makes them beholden

to shareholders shifting their primary focus away from a stable financial

system to maximizing share value and profit, not to mention executive bonuses.

This turns them into the very loan sharks they were supposed to eliminate.

Deregulation has been a universal neoliberal disaster. We

all know how hard it is to regulate ourselves, and we don’t have massive

profits involved. Self-regulation is no regulation, anarchy. Criminals thrive

in anarchy as do tyrants. Regulation limits and protects.

Just having a check done on your credit rating that isn’t

followed by a loan reduced your rating.

It is said that because most people are invested in banks

through pension funds and the like profit for banks is good for everyone. This

doesn’t justify the behaviour; it makes us complicit in our own exploitation,

in usury. Credits rating have become the chains of modern economic slavery.

Credit has replaced labour (defined as time and effort) as

the basis of our currency, for the money supply. Banks control credit and thus

money. They don’t sell goods and services; they control the financial system

and the value of currency. They determine who is in society and who is out because

you can’t do much these days without a bank account or credit card. Without a

banks account you8 have to pay fees to just get the money you earn. We are

supposed to be clients they advise not customers they exploit. Exploitation is

the basis of most retail.

Banks were permitted to exist to help regulate and infuse

cash into the system, not to skim off profit. This drains the economy and is

why when a financial industry grows too large, the economy suffers.Currency isn’t a good or service but a

representation of the labour used to produce such. It has no inherent value. It

shouldn’t be possible to make money off of money because this produces nothing

of real value, just an increase in abstract numbers. It is a trick of math and

the very definition of inflation. Things don’t demand more time or effort to

produce but everything gets more expensive because the currency itself has less

real value.The apparent growth in total

wealth is just an economic illusion.

The more complex, arcane, and opaque a system is, the more

likely it is to be based on utter nonsense or to be a screen for criminal

activity. Accounting is basic math: 1+1=2 not 2+10%. The current system is a literal

attempt to get money from nothing and that’s magical thinking not the basis of

a stable, productive economic system or society. It becomes trapped in the

inevitable boom and bust cycle of the stock market. Buy low and sell high. A financial

system needs to be reliable for its users than a casino. Right now banks are

the House. That’s why they record profits every year, despite the economic

reality around them. The House always wins.

If an enterprise is too big and essential to be allowed to

fail because of market conditions, it is too vital to be controlled buy those markets.

It is too big for private ownership and to be driven by market behaviour which

is short-sighted, opportunistic, and amoral. Because it is the basis of system,

it spreads throughout the system and society until there is no way to refuse, resistance

becomes futile and even nations must bow.

The financial industry has become a chain on the

transmission instead of a stabilizing lubricant. The engine is roaring,

overheating, and starting to cease in order to go nowhere fast while making a

damn loud noise. Banks don’t care as long we keep paying them for gas.

They even punish you with fees for responsible financial behaviour,

such as getting a credit card and not using it. Anything to push up the debit

and the profit, keeping you chained to the system.

It’s all for our benefit you know.

The sharks are only circling us for our protection.

Banks Are Spending Billions To Make Rich People Richer

Big banks have blown $157.4 billion buying up their own stock since the financial crisis.

The

CEO of America’s largest bank made a startling announcement last week:

His company has too much money, and he plans to throw away its profits

on rich people.

He didn’t quite put it that way, of course. In

his annual letter to shareholders, JPMorgan Chase CEO Jamie Dimon

boasted about his company buying $25.7 billion of its own stock over the

past five years, and hinted it could buy back another “big block of

stock this year” to further boost share prices.

At

their best, stock buybacks (also known as “share repurchases”) are

essentially pointless. At their worst, buybacks drain resources from

productive economic activity to provide a cheap high for Wall Street.

Companies buy their own stock to raise the stock price: Removing shares

from the market elevates the value of those that remain. Money is

funneled from corporate coffers to shareholders.

Companies

could, of course, do other things with their profits. They could raise

pay for their employees or provide better benefits. They could develop

new product ideas or upgrade old equipment to improve future production.

The point of a company, after all, is not simply to generate and

distribute cash, but to solve problems for society, or at least invent

cool stuff that makes life more interesting and fun. This doesn’t have

to be altruistic ― inventing awesome stuff raises stock prices when the

awesome stuff sells.

Alissa Scheller/The Huffington Post

Buybacks

overwhelmingly benefit rich people. Less than 22 percent of Americans

own $25,000 or more in stock, even through retirement accounts,

according to research

from New York University economist Edward N. Wolff. Those who own lots

of stock are heavily concentrated at the top. More than 92.8 percent of

households making at least $250,000 a year own at least $10,000 in

stock, compared with just 19.1 percent of households earning between

$25,000 and $49,999. Households in the top 1 percent receive an average

of 36 percent of their income from capital gains (stocks, bonds and

other financial investments), according to the Congressional Budget Office, while those in the lowest 20 percent receive an average of about 5 percent of their income this way.

Some

of the wealthy people who benefit most from buybacks are corporate

CEOs, who generally receive most of their compensation in stock.

To

fuel the economy, banks don’t have to make or invent anything that

people use. They just have to extend financing to people who want to

make stuff, or to people who want to buy it. This isn’t charity ― banks

earn big profits by lending.

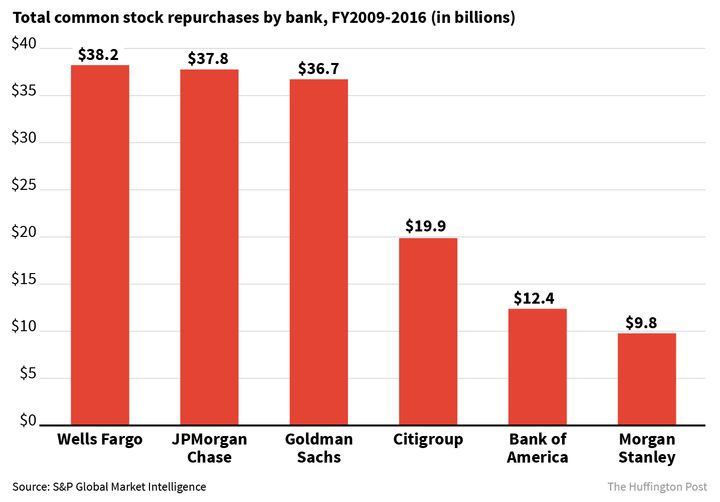

But

sometimes they’d rather just buy their own stock. Since the financial

crisis, the nation’s six largest banks have spent a combined $157.4

billion buying up their own stock, according to data from S&P Global

Market Intelligence. JPMorgan, Goldman Sachs and Wells Fargo have spent

over $36 billion each. All six of those banks declined to comment for this article.

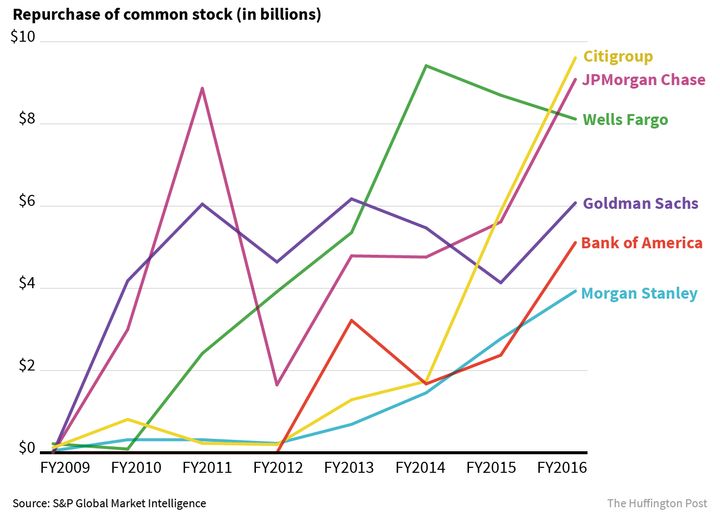

Defenders

of stock buybacks argue they can be a useful corporate strategy in a

weak economy. If companies can’t find a market for their products, then

placating investors through buybacks isn’t a terrible use of funds until

the economy turns up. Big Bank buybacks don’t fit that pattern ―

they’ve expanded tremendously during the last five years of economic

recovery, nearly quadrupling from $10.6 billion in 2012 to $41.9 billion

in 2016.

Alissa Scheller/The Huffington Post

Dimon’s

annual missives aren’t really for his shareholders ― they’re public

political statements from America’s most prominent banker. In the latest

edition, he noted that trillions of dollars in war spending, mass

incarceration and the student debt explosion have damaged the economy.

But while he didn’t offer specific policy remedies for those political

problems, he did make recommendations on economic policy, arguing that

excessive capital and liquidity regulations are tying up money his bank

could deploy to put people to work.

Dimon

called for weakening these rules, which require banks to rely on less

debt and hold more cash in case of trouble. Maybe it’s true that not one

dollar of the more than $9 billion JPMorgan spent on buybacks in 2016

could have gone toward making a good loan to a creditworthy business.

But if so, weakening capital and liquidity rules won’t help banks get

more money out the door ― the economy is just out of good lending

opportunities. In that scenario, JPMorgan would have nothing productive

to do with the money freed up by weakening capital and liquidity rules.

The broader economy would be shouldering more risk in order to further

enrich wealthy bank shareholders without seeing any increase in lending.

Big

banks have a history of being reckless with buybacks. Citibank

swallowed up over $7.5 billion of its own stock in 2006 and 2007, before

it needed a government bailout, as University of Massachusetts Lowell economics professor William Lazonick noted

in 2008. Morgan Stanley spent over $7 billion on buybacks over the same

period before it too needed to be bailed out. Bear Stearns spent $6

billion before needing a government-backed rescue from JPMorgan. Lehman

Brothers spent over $5 billion before missing the bailout train and

going bankrupt.

It’s one more way Wall Street fuels economic inequality.

Zach Carter is a co-host of the HuffPost Politics podcast “So That Happened.” Listen to the latest episode, embedded below:

Former CIBC representative says '85% of sales staff' in her workplace forged documents, encouraged by manager

By Erica Johnson, CBC News Posted: May 31, 2017 5:00 AM ET Last Updated: May 31, 2017 7:02 AM ET

'Signature falsification' was the primary allegation in 130 cases opened last year by the Mutual Fund Dealers Association of Canada. (Natalie Holdway/CBC)

About The Author

Erica Johnson

Investigative reporter

Erica Johnson is an award-winning investigative journalist. She hosted CBC's consumer program Marketplace for 15 years, investigating everything from dirty hospitals to fraudulent financial advisors. As co-host of the CBC news segment Go Public, Erica continues to expose wrong-doing and hold corporations and governments to account. Go Public

Employees in Canada's financial industry are speaking out about falsifying documents, telling Go Public that potentially criminal acts — like forging and photocopying customer signatures, adding initials to blank documents and using Wite-Out to conceal information — are more common than most people would think.

"It was easily 85 per cent of the back sales team doing it," says a former CIBC financial services representative, who worked in several bank branches and noted that forging signatures on documents occurred at all her workplaces. CBC has agreed to conceal her identity.

'You feel pretty awful knowing that you could have caused some serious harm to [customers] all in the name of profit for a bank.' - Former CIBC employee

The former employee, who left the bank last spring, says when she couldn't meet sales targets, her manager told her to forge customers' initials so it appeared that they had agreed to purchase insurance when they applied for a credit card, then cancel it a week or so later.

She also says a financial adviser who handled wealthy clients asked her almost two dozen times to forge customer signatures for insurance on loans, telling her his clients would never notice extra charges.

She says she finally quit because of stress and growing remorse.

"You feel pretty awful knowing that you could have caused some serious harm to them [customers] all in the name of profit for a bank."

This former CIBC financial services representative says a manager told staff to forge customer signatures to increase sales revenues and 'make the branch look good.' (Keon Chung/For CBC)

CIBC declined an interview request, but a spokesperson said in a statement that "the kind of behaviour described would be unacceptable and result in immediate termination. We take any allegation of this nature seriously and investigate thoroughly."

A financial adviser who recently left TD Bank says he often witnessed his manager copying customers' signatures onto documents using "signature cards" on file.

Been wronged? Contact Erica and the Go Public team

He himself would scribble over the dates on people's credit checks, and then black out the scribbles with thick felt pen so no one could tell he pulled an Equifax report without a customer's knowledge — a practice he says his manager demonstrated on a blank piece of paper.

"They were showing you [how to do it], they were teaching you. But they would never say that they told you to do so," says the former TD employee.

TD Bank also declined an interview but said in a statement that it takes the allegations "very seriously" and such behaviour "would be a significant breach of our code of conduct" subject to disciplinary action, including dismissal.

Cases of signature falsification on rise

In its annual enforcement report released last week, the Mutual Fund Dealers Association of Canada (MFDA) says "signature falsification" was the primary allegation in 130 cases opened last year — more than double the number of cases in 2015, and almost three times the number it investigated in 2014.

Financial consultants usually forged signatures for the client or consultant's "convenience," the report says, and the number of forgery cases has increased due to improved detection by compliance departments within financial firms.

The number of cases of signature falsification has almost tripled between 2014 and 2016. (Natalie Holdaway/CBC)

The problem of forging signatures was concerning enough for the MFDA to issue a bulletin in January — an update to similar bulletins issued in 2007 and expanded on in 2015.

It listed the deceptive methods people in the industry are using and warned against them, including copying a client's name on a document, cutting and pasting a signature, photocopying to "re-use" a signature, or using correction fluid to alter information on a document without a client's consent.

Although people in the financial industry have been found guilty of falsifying documents in recent years, few have served jail time or paid hefty fines.

"Forgery is supposed to be a criminal offence," says Stan Buell, of the Small Investor Protection Association. "But you could count on the fingers of one hand the people who have been charged criminally or sent to jail. It doesn't happen."

'It's not right to cheat old people'

Ten years ago, 97-year-old Harold Blanes says he asked his financial consultant to put about $400,000 of retirement savings into GICs — a safe investment, with no risk.

"We didn't want risk," the Kelowna man says. "We wanted our money saved, so we could enjoy it and help the kids with what they needed."

Harold Blanes, 97, says his former financial consultant doctored documents to put him in risky investments, earning her big commissions. (Gary Moore/For CBC)

Blanes says his financial consultant ignored a box he had ticked and initialled, indicating he only wanted to invest his savings for a short term. Instead, documents show that the box next to it was marked with a squiggly line — supposedly someone's initials, says Blanes — allowing the consultant to invest his money for six years.

She ended up putting it into mutual funds that tanked when the market crashed in 2008.

"She said over and over it was all in guaranteed investments," says Blanes. "And we had nothing to worry about."

After years of fighting with those managing his money, Blanes's initial investment was returned. He is now taking his financial consultant to court, estimating he has lost $136,000 in compound interest.

"It's not right at all to cheat old people out of their money," says Blanes. "I think it's disgraceful."

His son, Alan Blanes, says he thinks regulators need to crack down on financial employees who fudge documents and forge signatures.

"Dad's had 10 years of his retirement ruined by having to obsess over this case."

'They're trying to keep the genie in the bottle'

Ottawa-based lawyer Harold Geller says he is contacted by "hundreds of people a year" who say those giving them financial advice have lied, cheated and, in many cases, falsified documents and forged signatures in order to line their own pockets or boost a bank or investment firm's revenues.

Geller blames the MFDA for not taking a more aggressive approach, taking issue with the association's claim that forgery is mostly done for "convenience."

Lawyer Harold Geller says he's heard from clients who have been 'financially devastated' by forged and falsified documents. (Doug Husby/CBC)

"The Mutual Fund Dealers Association is a conflicted regulator," says Geller. "They are run by dealers and it's not in the dealer's interest to look into this issue. If there is not a complaint, [rarely] is this sort of thing looked for or caught."

Even when shady practices are caught, Geller says it can take about two years to reach a settlement; five years if the case goes to court. Either way, he says, investors are often muzzled by a confidentiality agreement.

"I think that they're trying to keep the genie in the bottle," he says. "If more people knew about the settlements that are available, there'd be more people looking for justice."

Calls for public inquiry

In a report released today calling attention to the issue of forgery, the Small Investor Protection Association says there is "absolutely no doubt" that the practice of document falsification is widespread.

"The truth is Canadians are losing billions of dollars of their savings every year due to systemic fraud and wrongdoing by the regulated investment industry," the report reads.

Buell says SIPA wants a government inquiry into investor protection.

"And they have to talk to the victims — not just the industry and regulators, and people who've done studies," he says. "Forgery is indicative of the behaviour of the investment industry."

Meanwhile, the former CIBC employee who routinely forged signatures says she's relieved to have left banking.

"But I actually feel fear for some of the new people entering the industry," she says. "Because there's a very big chance that they have no idea about what they are about to walk into."

A previous version of this story said the Mutual Fund Dealers Association of Canada issued a bulletin on signature forging in January that was an update to similar bulletins sent out in 2007 and 2010. In fact, it was an update to similar bulletins issued in 2007 and 2015.

May 31, 2017 6:27 AM ET

THE BLOG

08/05/2016 12:33 am ET | Updated Aug 05, 2016

Getting U.S. Dollars for Less: What the Banks Aren’t Telling Canadians

The first thing many Canadians do before crossing the border is visit the local bank and exchange their hard-earned loonies for a handful of US greenbacks. While this method of converting currency comes with the advantage of convenience, it certainly doesn’t come free. Canadians actually pay a hefty premium for the privilege of doing business with a financial institution every time they need to exchange Canadian dollars for U.S. funds.

When it comes to local currency exchange, it’s important to recognize there are two sets of exchange rates. There is the Bank of Canada published rates that you can find online and in the newspaper, then there are the exchange rates your bank actually uses when you buy U.S. cash with Canadian currency. One of these things is definitely not like the other.

The lower published rates reflect what banks use when they exchange enormous sums of money amongst themselves, the rates they charge us are typically as much as 3% higher. That’s because they add in what’s known as an exchange or conversion fee, that we don’t see. This billed to cover the cost of doing business at the retail level.

Exchange rates fluctuate from one financial institution to the next and are typically set by the individual banks themselves, because the fees included in these rates are intended to offset everything from the initial expense of buying foreign currency, to the administrative costs involved in making that currency available to us through bank branches and ATMs. Banks have a lot of administrative costs.

What many Canadians don’t realize is there’s a convenient way to get their U.S. dollars for less. If you only make the occasional cross-border shopping trip, an alternative foreign exchange option might not benefit you all that much. But for anyone who frequents the States on a regular basis, or who spends a significant amount of time there when they do go, the savings potential offered by taking advantage of a foreign currency exchange service can be significant.

Foreign exchange companies, like Knightsbridge Foreign Exchange Inc., offer lump sum online exchanges at rates that are significantly less than what the big banks charge. This is great news if you exchange your Canadian funds on a regular basis, or if you exchange large amounts of money at a time: think anyone who covers their child’s American tuition, pays the mortgage on a U.S. vacation property, or is one of the millions of Canadians who travel to Florida each winter.

In the case of a company like Knightsbridge, effectively competing with the big boys means combating the banks’ huge, hidden fees with exchange rates that are as much as 1.5% to 2.5% lower - even after the firm’s low commission fee is tacked on.

“The banks have an oligopoly and don’t compete on price, we are keeping them honest and helping Canadians save,” according to Rahim Madhavji, president of Toronto’s Knightsbridge Foreign Exchange, a firm he co-founded after quitting his job at the Royal Bank of Canada in 2009.

The entire premise is based on an ability to buy foreign currency in bulk, just like the banks do. Regardless of your bank’s rate, Knightsbridge guarantees they will beat it, and they will do it while offering same-day delivery of funds through bank transfers or online bill payments.

The basic process for working with Knightsbridge involves setting up a free online account, receiving written confirmation of your exchange rate before funds are transferred, then having the converted funds sent to the desired destination. Knightsbridge is also integrated with all Canadian banks, meaning that account-to-account transfers are free. According to Madhavji, the average customer can expect to save anywhere from a couple of hundred to several thousand dollars, depending on the amount of money exchanged.

The Canadian Snowbirds Association is another service that offers better-than-bank rates through online transfers. Much like Knightsbridge, the Snowbirds buy currency in bulk, but they do it by pooling their participants’ resources each month to get better exchange rates. The Association’s monthly transfer program involves moving money from your Canadian bank account to your U.S. bank account. They then charge members and non-members alike a transaction fee to facilitate this, as well as a fee to enroll in their program.

Knightsbridge offers a monthly currency buying program too, but the firm also gives customers the flexibility to purchase U.S. dollars any day of the week. For added convenience, you can register to be notified remotely whenever the dollar reaches a more favorable level.

It may be true that the ball is firmly in the banks’ court when it comes to the setting of U.S. exchange rates, but companies like Knightsbridge are putting the power of bulk buying into the hands of the individual, and in doing so, are giving Canadians the opportunity to beat the banks at their own game. Follow Stephanie R. Caudle on Twitter: www.twitter.com/stephrcaudle

Alissa Scheller/The Huffington PostBuybacks overwhelmingly benefit rich people. Less than 22 percent of Americans own $25,000 or more in stock, even through retirement accounts, according to research from New York University economist Edward N. Wolff. Those who own lots of stock are heavily concentrated at the top. More than 92.8 percent of households making at least $250,000 a year own at least $10,000 in stock, compared with just 19.1 percent of households earning between $25,000 and $49,999. Households in the top 1 percent receive an average of 36 percent of their income from capital gains (stocks, bonds and other financial investments), according to the Congressional Budget Office, while those in the lowest 20 percent receive an average of about 5 percent of their income this way.Some of the wealthy people who benefit most from buybacks are corporate CEOs, who generally receive most of their compensation in stock.

Alissa Scheller/The Huffington PostBuybacks overwhelmingly benefit rich people. Less than 22 percent of Americans own $25,000 or more in stock, even through retirement accounts, according to research from New York University economist Edward N. Wolff. Those who own lots of stock are heavily concentrated at the top. More than 92.8 percent of households making at least $250,000 a year own at least $10,000 in stock, compared with just 19.1 percent of households earning between $25,000 and $49,999. Households in the top 1 percent receive an average of 36 percent of their income from capital gains (stocks, bonds and other financial investments), according to the Congressional Budget Office, while those in the lowest 20 percent receive an average of about 5 percent of their income this way.Some of the wealthy people who benefit most from buybacks are corporate CEOs, who generally receive most of their compensation in stock. Alissa Scheller/The Huffington Post

Alissa Scheller/The Huffington Post

No comments:

Post a Comment